Sometimes, the summer heat gives us a rare moment to pause and, hiding in the cool shade, reflect on the path we’ve taken since the start of the year. As far as space is concerned, the first half of 2025 has been record-breaking in two key areas: the rapid acceleration of satellite deployment and testing.

The main areas of interest have remained the Moon (and all types of space operations contributing to its exploration), satellites (the pace of deployment of nearly all players has been astonishing since the beginning of the year), and space weaponry, which is increasingly leveraging the capabilities of artificial intelligence (AI) systems. So let’s take a closer look at these in a briefing on the year’s most significant developments.

The Moon: CLPS is gaining momentum but still searching for new contractors

An ambitious Moon program began last year with the launch of NASA’s Commercial Lunar Payload Services (CLPS) program and continued in January with the launch of a Falcon 9 rocket. Alas, the 365,000 km space marathon didn’t end well for all the “passengers” aboard.

Among those who succeeded was the Blue Ghost lunar lander from Firefly Aerospace. The spacecraft, launched under NASA’s CLPS program, touched down on the Moon’s surface on March 2, 2025. The mission delivered scientific experiments and commercial cargo to Earth’s satellite and operated continuously for 14 days, successfully achieving all its objectives.

Source: sodern.com

Alongside Blue Ghost, the Japanese Hakuto-R Mission 2 lander, developed by ispace, launched aboard the same Falcon 9 rocket on January 15. Unfortunately, unlike Firefly Aerospace’s lander, it was unsuccessful: on June 5, it failed during landing and ultimately crashed on the lunar surface.

Another lander under NASA’s CLPS program, IM-2 from Intuitive Machines, also attempted to descend to the Moon on March 6, 2025. However, it tipped over onto its side, though it did maintain partial radio contact. The CLPS program was expected to feature the launch of Blue Origin’s Blue Moon Pathfinder, but it was rescheduled for 2026.

Source: NASA

The mission will serve as a test flight for Blue Origin’s Blue Moon Mark 1 lander and will also carry commercial payloads. Some of these modules are expected to test core technologies for the upcoming Human Landing System (HLS). Blue Moon will be the primary spacecraft tasked with returning humans to the Moon under NASA’s Artemis program.

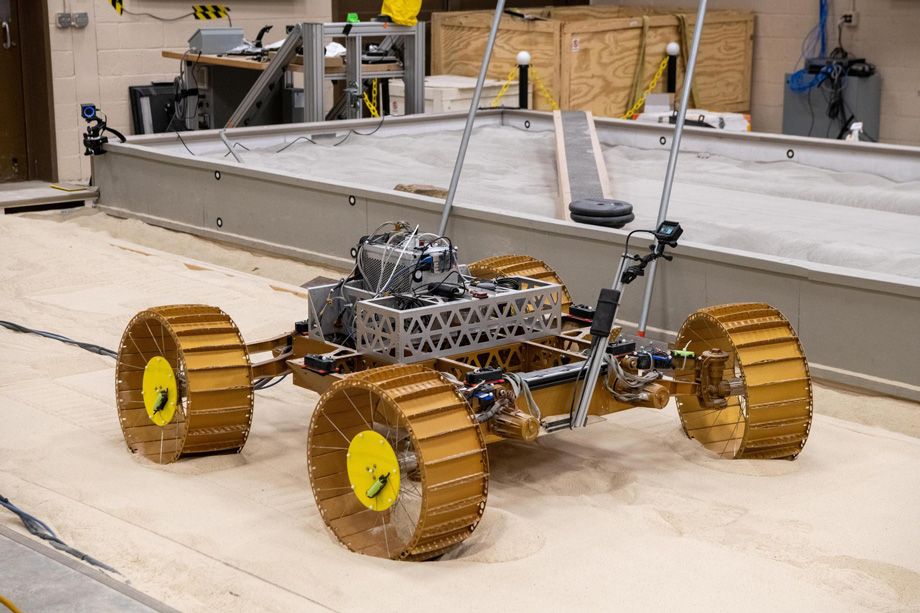

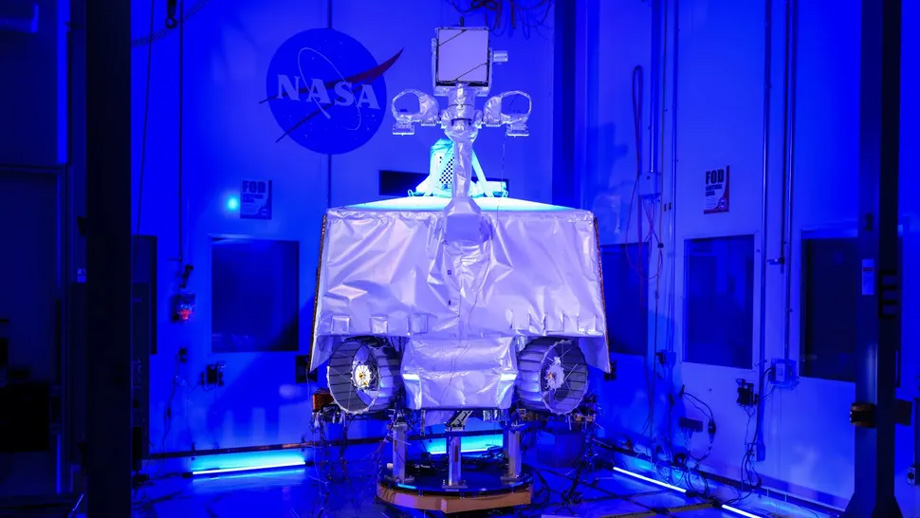

In February 2025, news emerged about the partial revival of another CLPS space mission: Griffin Mission 1, implemented by Astrobotic Technology. NASA canceled this mission in 2024 due to a significant budget overrun. The majority of the costs were linked to the lander’s primary payload, the Volatiles Investigating Polar Exploration Rover (VIPER).

The wheeled rover was originally planned to begin its 100-day mission in the fall of 2025, searching for water ice near the Nobile crater. However, its original $84 million cost ballooned to $450 million during development. 96% of that sum, $433.5 million, was due to the cost of VIPER alone, meaning that each kilogram of this 430-kg spacecraft ended up costing over a million dollars.

Source: NASA

Source: NASA

VIPER’s cost was such that NASA realized that, relying solely on budget funding, the platform was simply not feasible. However, the space agency urgently needed to demonstrate the Griffin lander platform’s capabilities.

To solve this dilemma, NASA offered the fully assembled and flight-certified rover free of charge to any partner company capable of organizing the entire space mission cycle, from launch and deployment to data collection and transmission back to Earth. As of late July 2025, no such contractor had come forward. Still, the agency’s strategy is pleasantly surprising: rather than mothballing a fully flight-ready rover or dismantling it for spare parts, it opted for an approach that might just give VIPER a second shot at life.

While NASA continues searching for a well-funded and capable steward for VIPER, it also hinted that the loss of the mission’s primary payload shouldn’t delay the launch of the Griffin lander. Many are eager to see what this core spacecraft can do, and its successors are expected to provide long-term logistical support for humans on the Moon.

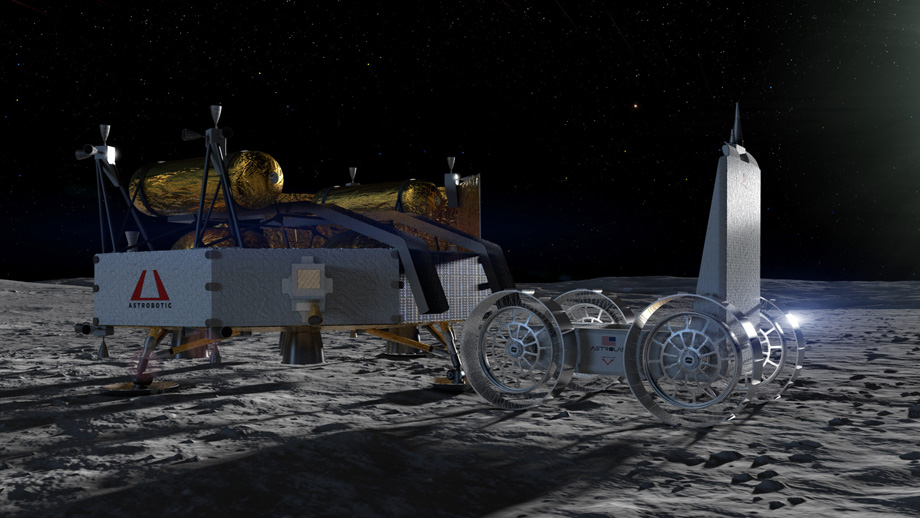

To maintain the rocket’s pre-calculated trajectory and fuel usage, the rover’s mass will be replaced with a mock-up platform: the FLEX Lunar Innovation Platform (FLIP), which Astrobotic Technology quickly developed as a substitute. FLIP is intended to be the forerunner of Astrobotic’s full-scale rover, the Flexible Logistics and Exploration (FLEX), which the company plans to send on future Griffin missions.

Source: astrobotic.com

The story of Griffin 1’s swift revival suggests that NASA is beginning to adapt to the realities of the tough budget constraints that have plagued it for years. This new approach allows large government space agencies like NASA to save taxpayer money on secondary projects while simultaneously incentivizing new contractors.

Increasingly, NASA is shifting to a “Space-as-a-Service” model, in which the agency acts essentially as a client, purchasing services (launches, cargo deliveries, even habitation on commercial space stations) from partner companies that serve as operators.

As of 2025, engineers are actively working to establish a sustainable cargo delivery system to the Moon for a wide range of purposes, from resource extraction platforms to in-situ utilization, such as producing rocket fuel or oxygen supplies.

Since the beginning of the year, we’ve seen a genuine competition emerge among manufacturers developing planetary landing platforms. These range from simplified designs for observation to heavier cargo carriers capable of delivering small rovers, ice-hunting stations, or other types of lunar infrastructure. All these efforts are united by a common goal: building a logistical hub on the Moon’s surface, which humanity will one day rely on for deep space missions.

China targets asteroids and comets

Another noteworthy space launch in the first half of 2025 was the Chinese Tianwen 2 (ZhengHe) mission, which took place in late May. The goal of this mission is to return samples from the asteroid 469219 Kamoʻoalewa to Earth and to conduct detailed research on the main-belt comet 311P/PANSTARRS over a decade. This mission is part of the broader Chinese program for exploring the Solar System, called Planetary Exploration of China (PEC), or simply Tianwen.

Source: CASC

The uniqueness of Tianwen 2 lies in its dual activity: the collection of asteroid samples and the flyby of another comet will be carried out as part of a single mission. None of the previous remote exploration programs for comets or asteroid sample return missions conducted by NASA (OSIRIS-REx), ESA (Rosetta), or JAXA (Hayabusa and Hayabusa 2) have attempted to perform both tasks in one mission.

Tianwen 2 launched on May 28, 2025, as flashes from the Long March 3B/E rocket engines cut through the night sky above the Xichang Space Center. The spacecraft is expected to arrive at asteroid 469219 Kamoʻoalewa in July 2026. This will be followed by 9 months of studying the celestial body, culminating in an attempt to collect samples and return them to Earth. During a close flyby of our planet in November 2027, Tianwen 2 is scheduled to release a return capsule containing the collected samples. After that, the probe will head toward the mission’s next target, comet 311P/PANSTARRS. That journey is expected to last about seven years.

Source: nasaspaceflight.com

With Tianwen 2, China has joined the missions aimed at returning samples from other celestial bodies in the Solar System to Earth. It is also worth noting the active expansion of the role played by the Chinese Tiangong Space Station (TSS). With it, China is testing its own technologies for crew delivery to orbit, spacecraft, spacesuits, and more.

During the mission of the Shenzhou 20 spacecraft, which launched on April 24, 2025, two successful spacewalks by the crew were undertaken. TSS thus continues to serve as a reliable platform for scientific research by taikonauts, particularly in the fields of human physiology, Earth observation, and robotics. It is from here that China’s first steps toward space colonization begin.

Source: aa.com.tr

As of mid-2025, Beijing is also developing a range of new spacecraft to facilitate a sustainable presence on the Moon. The primary launch vehicle has already been chosen as the Long March 10 rocket. In March 2025, successful testing of the new-generation YF-100K main engines took place.

The manned spacecraft for trans-lunar flights will be Mengzhou. In June 2025, an important test of its emergency escape system (a pad-abort test) was completed. Mengzhou is ultimately expected to deliver the Lanyue lunar lander, inside which a crew of taikonauts will reside, to lunar orbit. For extravehicular activities, taikonauts will wear Wangyu lunar spacesuits, which are currently in the early stages of development. The tentative start date for China’s permanent manned lunar missions is set for the beginning of the next decade.

China also plans to launch (or may have already covertly launched) 2-3 quantum communication satellites into low Earth orbit during 2025. This is primarily aimed at advancing quantum key distribution (QKD) technologies and developing a global quantum communications network. At the same time, the country continues to expand its own broadband satellite megaconstellations: the Chinese are intensively launching new Guowang and Qianfan satellites monthly, positioning them as key non-American competitors to Starlink. The rapid deployment of these constellations is part of China’s global strategy to strengthen its digital economy and ensure global communication services. But it’s not just the Chinese experiencing a true satellite boom this year.

Strengthening satellite constellations amid the growing militarization of space

Since the beginning of the year, it has been clear that orbital deployments would only accelerate and the pace would be explosive. By May 2025, the number of active satellites around Earth had increased by a third compared to the start of the year. By the end of 2025, the number of operational satellites around Earth may approach 13,000.

The intensity of satellite fleet expansion was especially noticeable among private giants: in just seven months, SpaceX had already carried out 87 rocket launches, deploying 1,320 of its own satellites into orbit. Among them are nearly 1,000 satellites in the Starlink megaconstellation alone. At the beginning of the year, in January, there were about 6,850 Starlink satellites, a number that has already grown to 9,394, after the last launch on August 14.

Source: SpaceX

If we count all the spacecraft launched into space by Elon Musk’s company, the number approaches 1,700. That’s about three-quarters of all satellites deployed by all countries during the first half of 2025. Indeed, the scale of SpaceX’s monopoly on space launches remains astonishing, even in 2025.

Other factors explaining the satellite deployment boom are tied to global tensions in which all major space powers are now involved to varying degrees. This pressure is pushing countries to more actively develop new space systems and to reassess the use of older, already deployed ones. That’s why the Pentagon remains deeply invested in Elon Musk’s space capabilities and satellite resources. Today, Starlink is firmly integrated into the U.S. military and government communications network.

In addition, by the end of the year, SpaceX is expected to triple the number of active satellites for the United States Space Force (USSF), expanding it from 50 to 150. The new spacecraft will be used for Earth monitoring, observation, and the provision of secure communications, including strategic SATCOM channels. One hundred new satellites for the USSF may seem like a lot, but it’s important to remember that the new strategy of building more resilient and distributed networks heavily involves private communication satellites in data collection and transmission. That means this year’s expansion of the American satellite constellation also includes the already-deployed Starlink satellites, along with those from other satellite companies contributing to national security.

Such dual-use satellites are being deployed not only by the U.S. but also by China. Chinese satellites in low and geostationary Earth orbit are increasingly demonstrating advanced maneuvering capabilities, raising concerns about their potential use in space conflicts. Beijing, in a mirror image of Washington, continues to increase the number of space launches that may have military applications. This especially applies to the previously mentioned Starlink analogues, the Qianfan (formerly known as G60 “Starlink”) and Guowang megaconstellations. Together, they aim to deploy tens of thousands of active satellites into Earth orbit for broadband coverage.

Overall, 2025 is proving that the rapid expansion of both civilian and military space capabilities is a high-stakes game between China and the United States.

Business: What does space money smell like these days?

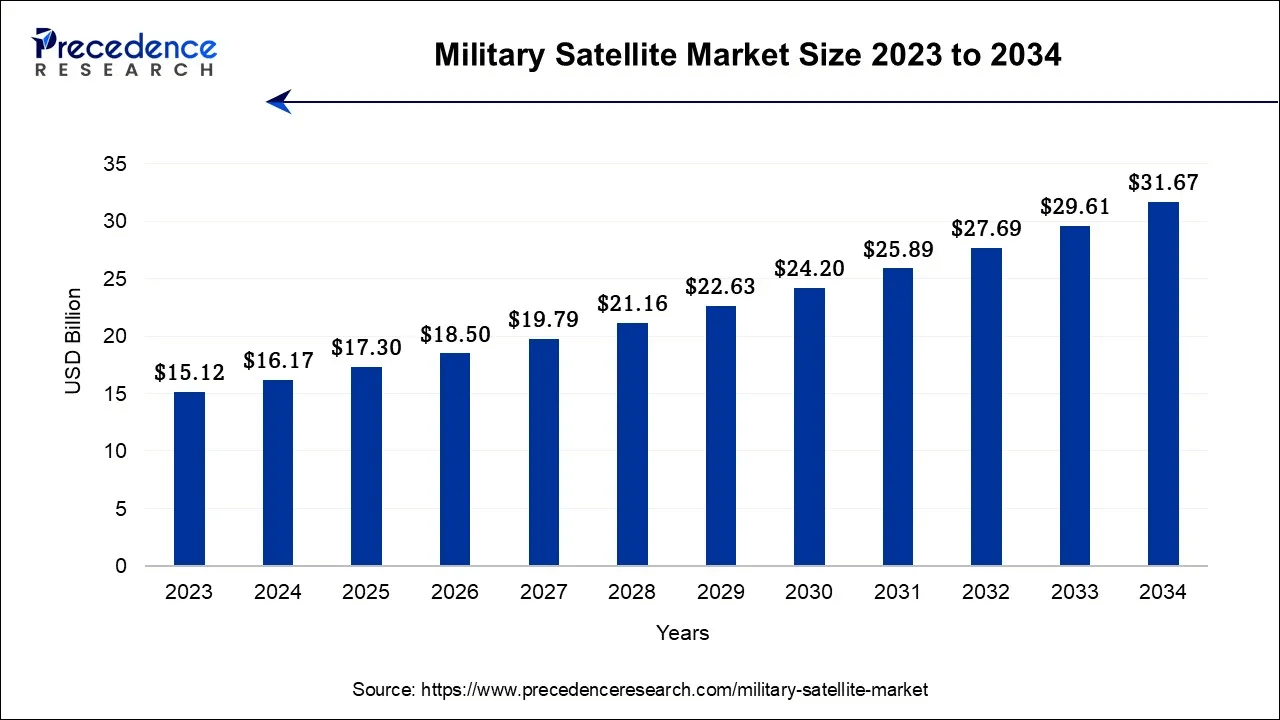

The trend toward increasing militarization in space as of 2025 is best illustrated by growing investment numbers, particularly for defense-related space activities. According to estimates from Precedence Research, the global military satellite market is currently valued at $17.3 billion. A steady and significant influx of investment into this sector is expected to raise that figure to $27.69 billion by the end of 2032. However, the relentless escalation of military confrontations on Earth over the past year will likely drive further investments in this area.

Source: precedenceresearch.com

In the global business arena, the first half of 2025 saw a 9% decline in merger and acquisition (M&A) activity compared to the same period in 2024. However, alongside the drop in the number of deals, their total value rose by 15%, indicating a shift toward larger and possibly more strategic transactions. Given the heightened attention that defense departments worldwide are paying to the space sector, the trend becomes clearer even to the casual observer.

There was also a notable strengthening of public-private partnerships (PPPs) in space projects. One clear example of this approach is the situation with the VIPER rover, where NASA, instead of mothballing the completed spacecraft, decided to seek a potential project executor among its private sector partners. We are also seeing a growing role of national governments in supporting the space industry. In an environment of escalating geopolitical tension, states are moving the industry forward to secure reliable access to space services in case regional armed conflicts escalate into global war.

Over the past six months, domestic investment in the U.S. space sector has increased significantly. Buyers from both North and South America boosted their investments in space by 16% in the first half of 2025. Moreover, 91% of that capital stayed within the region, indicating a strengthening internal market. In the U.S., this can be explained by trends toward protecting the domestic space services market, as well as the need to develop national space infrastructure. A similar response may also have been shaped by announcements from the Trump Administration about its intent to deploy a new multi-layered national missile defense architecture called the “Golden Dome.”

The investment climate in the Asia-Pacific region has also improved significantly, particularly in the NewSpace sector and even relative to the Americas. Buyers from the Asia-Pacific region more than doubled their investments, which previously accounted for just 22% of the total value of their deals.

New directions for the development of the space business, along with its key challenges, were explored by participants and guests of the New Space Economy Congress, held in Barcelona on July 3–4. Among the many ideas discussed at the forum were debates over the implementation of new methods of sustainable development in space and the issue of space debris. These included conversations on active debris removal technologies and the creation of norms and regulations for the responsible use of orbit. Promoting the “green transition” through space technologies also continues to dominate such events.

Given the rapid deployment of Starlink and the equally ambitious plans of its main U.S. competitor, Amazon’s Kuiper internet constellation, the Congress also organized panel discussions on global connectivity and improving network resilience. One of the proposed approaches is the integration of satellite communication directly into mobile networks via Direct-to-Device (D2D) technologies. A wide range of satcom entrepreneurs also discussed new models for monetizing 5G and the future potential of the 6G mobile standard, which promises a thousand-fold increase in data transfer speeds.

Source: dreamstime.com

Many observers are predicting a strong “AI-centric” focus for the future 6G network, which will require dedicated tools for its implementation and support. Increasingly, it is evident that the space sector is taking a more serious approach to the adoption of AI-based methods. The role of artificial intelligence in automating and optimizing network operations and processing space data promises to far exceed all the computational capabilities we have at present. The use of such AI systems in processing space data for various sectors, including agriculture, logistics, infrastructure monitoring, and climate change mitigation, holds great potential and could significantly strengthen these segments of the space economy.

However, the most active zone of AI technology implementation remains the military sector. In May 2024, the U.S. Space Force signed a $1.2 billion contract to deploy 48 AI-controlled SAR satellites for the autonomous detection of mobile missile launchers. In Q4 2025, this deal is set to reach its initial operational capability phase, after which the first USSF SAR satellites, operated by AI systems, will begin to appear in orbit.

Japan also has plans to increase the number of its own SAR satellites, albeit on a smaller scale. A recent $950 million program announced by the country’s defense ministry envisions the deployment of 12 satellites in 2025, equipped with infrared sensors and AI processors to track hypersonic gliders and missiles. Officially, this is being done in response to regional threats. But considering that Japan never signed a peace treaty with Russia after World War II, such heightened situational awareness may serve as a kind of deterrent against potential acts of aggression.

Political statements by world leaders and the introduction of new types of ASAT (anti-satellite) weapons continue to fuel the militarized space market. On one hand, this period of tension presents additional opportunities to profit from launch vehicles. On the other hand, it brings with it a real risk of seeing orbital assets destroyed. For now, however, the involved parties continue expanding their space presence, with each claiming it is solely for reasons of national security.